Rising Insurance & Taxes in 2026: The Hidden Affordability Math Buyers Miss in TX, FL, and Beyond

Understanding the True Cost of Homeownership in High-Tax and High-Risk States

When planning to buy a home, many prospective buyers laser-focus on the principal and interest rate. However, as we approach 2026, the real affordability shock lies in the hidden math of rising property taxes and skyrocketing homeowners insurance premiums.

For buyers in states like Texas and Florida, failing to account for these localized costs can severely inflate monthly payments. Whether you are looking for a conventional loan in Austin, TX, or exploring financing options in Florida, understanding state-specific holding costs is critical.

At the Josh Brown Team, we believe in complete transparency. With over 25 years of experience providing tailored mortgage solutions across 11 states, we help our clients look beyond the base mortgage payment to ensure long-term financial stability.

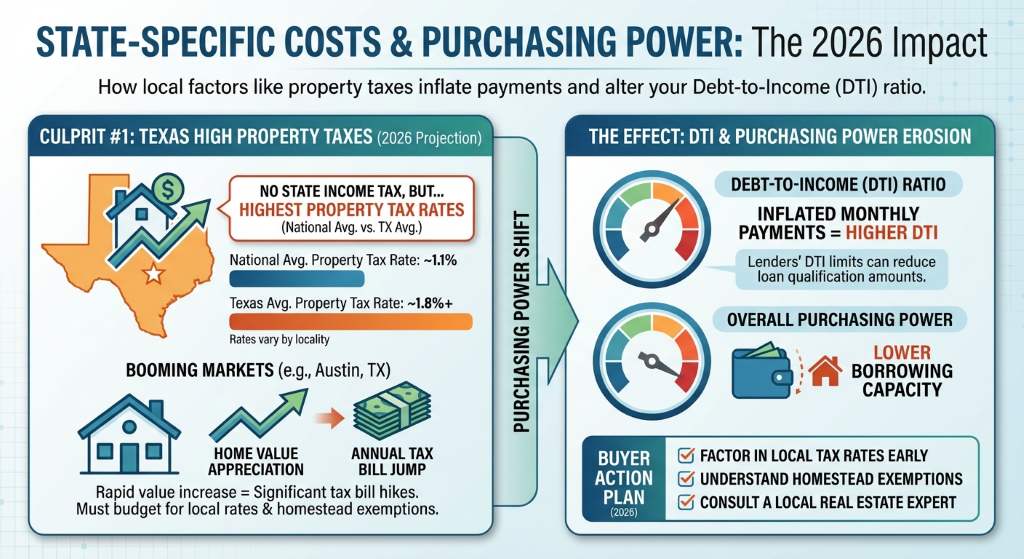

How Texas Property Taxes and Florida Hurricane Deductibles Impact Your Monthly Payment

State-specific costs can dramatically alter your debt-to-income ratio and overall purchasing power. Let us break down the two most significant culprits inflating payments in 2026:

- Texas High Property Taxes: Texas boasts no state income tax, but it compensates with some of the highest property tax rates in the nation. In booming markets like Austin, TX, rapid home value appreciation means your annual tax bill can jump significantly. Buyers must factor in local tax rates and understand how homestead exemptions work to mitigate these costs.

- Florida Hurricane Deductibles and Insurance Premiums: Florida residents face a uniquely volatile insurance market. With the increasing frequency of severe weather, insurers are hiking premiums and enforcing strict hurricane deductibles. These deductibles are often a percentage of the home value, requiring buyers to have substantial emergency funds on hand.

These escalating costs mean that a home priced at $500,000 in Texas or Florida will have a vastly different monthly carrying cost compared to a similarly priced home in a lower-tax state like Missouri or Arkansas. If you already own a home and are feeling the pinch of rising taxes, exploring refinance options might help you restructure your debt to absorb these increases.

| Cost Category (Estimated) | National Average | Austin, TX (High Tax) | Florida (High Insurance) |

|---|---|---|---|

| Home Purchase Price | $500,000 | $500,000 | $500,000 |

| Monthly Principal & Interest | $2,500 | $2,500 | $2,500 |

| Estimated Monthly Property Tax | $450 | $850 | $400 |

| Estimated Monthly Insurance | $150 | $200 | $450 |

| Total Estimated Monthly PITI | $3,100 | $3,550 | $3,350 |

Advanced Mortgage Qualification: Preparing for 2026 and Beyond

As lending standards adapt to these rising costs, advanced qualification factoring becomes essential. Lenders must now rigorously stress-test your budget against projected 2026 tax assessments and insurance renewals. Here is how you can proactively prepare:

- Use Accurate Estimates: Do not rely on outdated national averages. Utilize tools like our comprehensive Mortgage Calculator to input realistic local tax and insurance figures.

- Explore Specialized Loan Programs: Depending on your location and financial profile, certain loans offer more flexibility. We specialize in FHA loans for flexible credit requirements, VA loans for eligible veterans, and Jumbo loans for higher-value luxury properties.

- Partner with a Local Expert: Working with an experienced Austin, TX mortgage lender who is also licensed in states like Florida, Colorado, and Arizona ensures you have a guide who understands regional nuances.

Compliance Information: Josh Brown Team with Fairway Independent Mortgage Corporation. Josh NMLS: 216153. Company NMLS: 2289. 4501 Spicewood Springs Rd, Suite 1050, Austin, TX 78759. This is not an offer to enter into an agreement. Not all customers will qualify. Information, rates, and programs are subject to change without prior notice. All products are subject to credit and property approval.

Q1: Why are property taxes so high in Austin, TX?

Texas does not have a state income tax, so local governments rely heavily on property taxes to fund public services like schools and infrastructure. Rapid home appreciation in the Austin area has also driven up assessed property values.

Q2: How do Florida hurricane deductibles impact my mortgage?

Hurricane deductibles are often calculated as a percentage of your home value rather than a flat fee. Lenders factor these potential out-of-pocket costs and the high base insurance premiums into your debt-to-income ratio during qualification.

Q3: Will rising insurance and taxes affect my ability to get a conventional loan?

Yes. Because taxes and insurance are part of your total monthly housing expense, significant increases can raise your debt-to-income ratio, which may potentially lower your maximum loan approval amount.

Q4: Can refinancing help if my property taxes and insurance increase?

Absolutely. Refinancing your mortgage to a lower interest rate or an extended term can reduce your principal and interest payment, helping to offset the higher costs of taxes and insurance.

Q5: How can the Josh Brown Team help me navigate these rising costs?

With over 25 years of experience across 11 states, we provide advanced qualification factoring. We analyze localized costs upfront so you know exactly what your true monthly payment will be before you make an offer on a home.Schedule a Free Loan Consultation Today