Cash-Out Refi in Multi-State Markets 2026: Equity Strategies for Debt, Investments, and Emergencies

Navigating Home Equity Beyond Renovations in 2026

As we approach 2026, homeowners in Austin, TX, and across the nation are sitting on significant levels of home equity. While historically used for home improvements, a cash-out refinance is increasingly becoming a strategic financial tool for broader wealth management. Whether you want to consolidate high-interest debt, fund an investment property, or build a robust emergency reserve, tapping into your home’s equity requires careful scenario modeling and expert guidance.

For homeowners managing properties across different regions, understanding multi-state market dynamics is crucial. The Josh Brown Team at Fairway Independent Mortgage Corporation specializes in helping clients navigate these complexities. Operating in 11 states, including Texas, Florida, and Colorado, our team provides tailored mortgage solutions that align with your unique financial goals. By leveraging a cash-out refi, you can transform illiquid home value into actionable capital, provided you understand the specific rules governing your state.

State-by-State Nuances: Texas, Florida, and Colorado

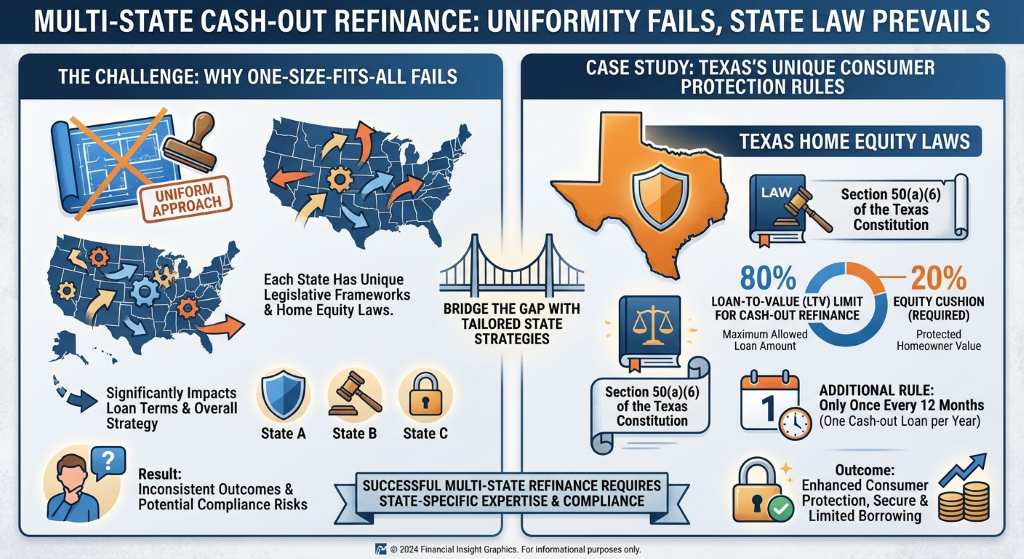

When planning a cash-out refinance in a multi-state market, a uniform approach simply does not work. Each state has its own legislative framework governing home equity, which can significantly impact your loan terms and overall strategy.

- Texas Home Equity Rules: Texas has some of the most unique consumer protection laws in the country. Under Section 50(a)(6) of the Texas Constitution, homeowners are limited to an 80% Loan-to-Value (LTV) ratio for cash-out refinances. Additionally, you can only execute a cash-out refi once every 12 months. This makes precision in your scenario modeling essential if your primary residence is in Austin, TX, or anywhere else in the Lone Star State.

- Florida Nuances: In Florida, homeowners must account for documentary stamp taxes and intangible taxes on new mortgages. While Florida does not have the strict 80% LTV cap found in Texas, these upfront closing costs mean that borrowers need to carefully calculate their break-even point before using equity for investments or debt payoff.

- Colorado Dynamics: Colorado offers a dynamic real estate market with rapid equity growth. The state allows for higher LTV limits on conventional loans, making it easier to pull larger sums of cash for purchasing secondary investment properties or funding major life events.

Partnering with an experienced multiple states market lender like Josh Brown ensures you avoid unexpected regulatory hurdles and secure the best possible terms for your location.

| State | Max LTV Limit (Typical) | Key Regulatory Nuance | Best Strategy Focus |

|---|---|---|---|

| Texas | 80% | Section 50(a)(6) once-per-year rule | High-interest debt consolidation |

| Florida | Up to 80-85% | Documentary stamp and intangible taxes | Long-term property investments |

| Colorado | Up to 80-85% | High conforming loan limits in key counties | Emergency reserves and wealth building |

Scenario Modeling: Best Uses and Avoiding Common Pitfalls

To maximize the benefits of a cash-out refinance in 2026, scenario modeling is a must. By comparing different financial paths, you can determine exactly how your home equity can work hardest for you.

- Debt Consolidation: If you are carrying credit card debt with interest rates exceeding 20%, rolling that debt into a mortgage with a significantly lower rate can improve your monthly cash flow. However, a common pitfall is extending short-term debt over a 30-year period without adjusting your spending habits.

- Investment Properties: Using equity from your primary residence to fund a down payment on a rental property is a powerful wealth-building strategy. This allows you to leverage existing assets to generate passive income, though you must ensure the rental yield outpaces your new mortgage payment.

- Emergency Reserves: In uncertain economic times, having liquid cash is invaluable. Pulling equity to create a safety net can provide peace of mind.

The key to success is working with a transparent, professional lender. Led by Branch Manager and Senior Loan Officer Josh Brown, our team has over 25 years of experience providing tailored mortgage solutions. We help you model these scenarios, factor in closing costs, and navigate multi-state regulations to ensure your equity strategy is sound and secure.

Q1: What is the maximum loan-to-value (LTV) ratio for a cash-out refinance in Texas?

In Texas, state law restricts cash-out refinances to a maximum of 80% of your home’s appraised value. This ensures homeowners retain at least 20% equity in their property.

Q2: Can I use a cash-out refinance to buy an investment property?

Yes, using a cash-out refinance to secure funds for a down payment on a second home or investment property is a very common and effective wealth-building strategy.

Q3: How does a cash-out refinance impact my current mortgage rate?

A cash-out refinance replaces your existing mortgage with a completely new loan. Your new interest rate will be based on current market conditions, your credit score, and the amount of equity you are extracting.

Q4: Are there restrictions on how I can use the cash from my equity?

Generally, there are no restrictions on how you spend the funds. You can use the cash for debt consolidation, investments, home renovations, or emergency reserves.

Q5: Why should I choose a multi-state lender like the Josh Brown Team?

Working with a lender licensed in multiple states (like our 11-state footprint) means we understand the specific tax laws, LTV limits, and regulatory nuances of different regions, ensuring a smooth and compliant financing journey.