The Ultimate Guide to Adjustable-Rate Mortgages in Austin, TX

- 3/1 ARM and 5/1 ARM: The rate is fixed for 3 or 5 years, then adjusts every 1 year.

- 7/1 ARM and 10/1 ARM: The rate is fixed for 7 or 10 years, then adjusts annually.

- 5/6 ARM and 7/6 ARM: The rate is fixed for 5 or 7 years, then adjusts every 6 months, a structure becoming increasingly common in today’s market.

These loans are particularly popular for buyers who plan to move or opt for a rate and term refinance before the introductory period ends. Whether you are buying a starter home or utilizing a jumbo mortgage for a luxury property, understanding these terms is the first step to making an informed financial decision.

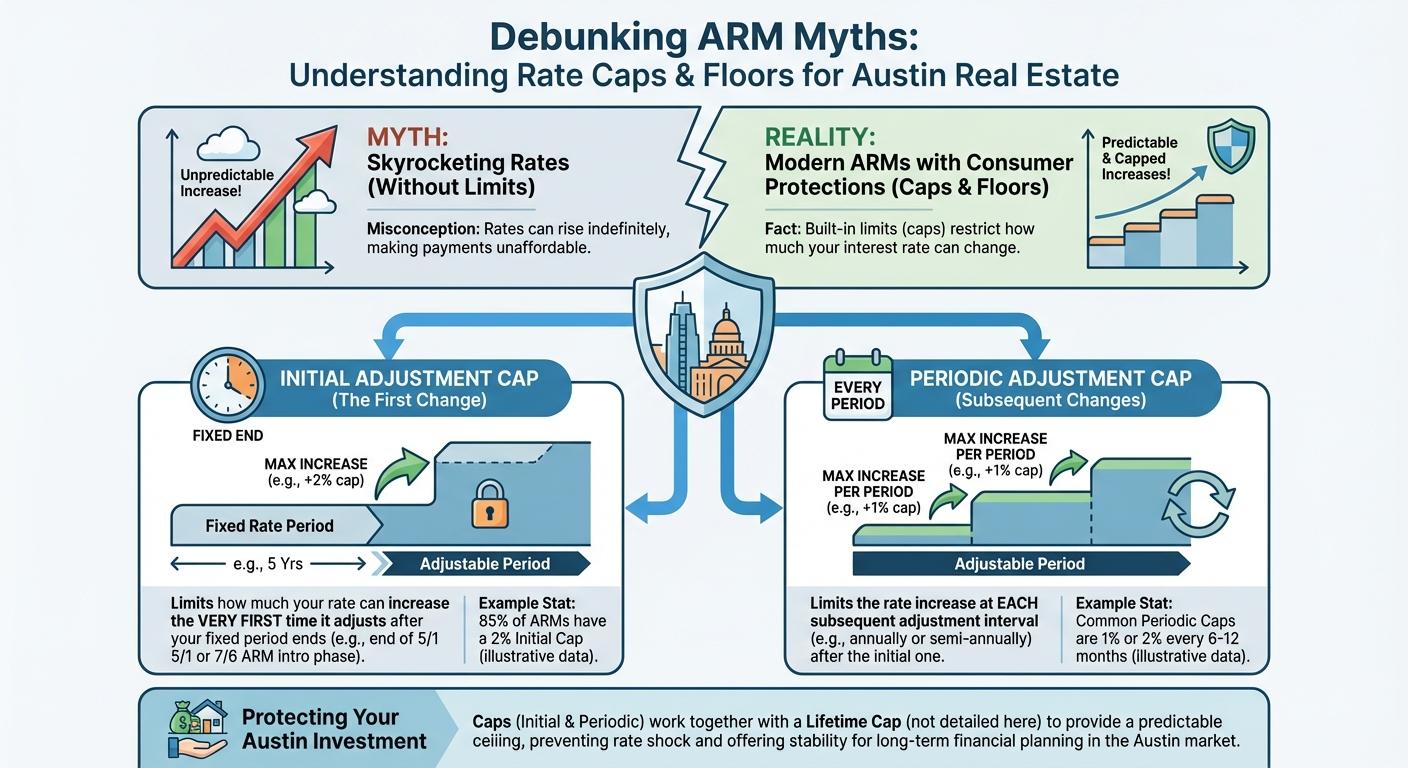

Navigating Caps, Floors, and ARM Adjustments

One of the biggest misconceptions about an adjustable rate mortgage is that the interest rate can skyrocket without limits. In reality, modern ARMs come with built-in consumer protections known as caps and floors.

Here is how they work to protect your Austin real estate investment:

- Initial Adjustment Cap: This limits how much your rate can increase the very first time it adjusts after your fixed period (for example, the end of your 5/1 ARM or 7/6 ARM introductory phase).

- Periodic Adjustment Cap: This restricts how much the rate can change during subsequent adjustment periods (usually annually or every six months).

- Lifetime Cap and Floor: The lifetime cap sets a strict maximum interest rate for the life of the loan, while the floor establishes the absolute minimum rate.

At the Josh Brown Team, we know that understanding the fine print of an adjustable-rate mortgage can feel overwhelming. That is why we are experts at providing second opinions on adjustable-rate mortgages. If you have been quoted a 5/1 ARM or 10/1 ARM by another lender, let our Austin-based team review the caps, margins, and indexes to ensure you are getting a highly competitive deal.

| ARM Type | Initial Fixed Rate Period | Adjustment Frequency |

|---|---|---|

| 3/1 ARM | 3 Years | Annually (Every 1 Year) |

| 5/1 ARM | 5 Years | Annually (Every 1 Year) |

| 5/6 ARM | 5 Years | Semi-Annually (Every 6 Months) |

| 7/1 ARM | 7 Years | Annually (Every 1 Year) |

| 7/6 ARM | 7 Years | Semi-Annually (Every 6 Months) |

| 10/1 ARM | 10 Years | Annually (Every 1 Year) |

Is an Adjustable-Rate Mortgage Right for Your Austin Home Purchase?

Choosing an adjustable rate mortgage depends heavily on your financial goals and timeline. If you plan to relocate from Austin, TX, upgrade to a larger home, or refinance within the next 5 to 10 years, a 5/1 ARM, 7/1 ARM, or 10/1 ARM could save you thousands in interest during those crucial early years.

However, if you plan to stay in your home for decades, a traditional fixed-rate loan might offer more peace of mind. As your trusted partners in home financing, the Josh Brown Team with Fairway Independent Mortgage Corporation is dedicated to clear communication and education. We will help you weigh the pros and cons of a 5/6 ARM versus a 7/6 ARM, ensuring your mortgage aligns perfectly with your lifestyle and budget.

Disclaimer: The Josh Brown Team is a branch of Fairway Independent Mortgage Corporation. Josh Brown NMLS: 216153. Company NMLS: 2289. Equal Housing Opportunity. All loan information is presented for educational purposes and does not constitute a commitment to lend.

Q1: What is an adjustable rate mortgage?

An adjustable-rate mortgage (ARM) is a home loan with an interest rate that can change periodically. This means that the monthly payments can fluctuate over time based on market conditions.

Q2: What does 5/1 ARM or 7/1 ARM mean?

The first number indicates the number of years the initial interest rate is fixed. The second number indicates how often the rate can adjust after the fixed period. For example, a 5/1 ARM is fixed for 5 years and adjusts every 1 year thereafter.

Q3: How does a 5/6 ARM differ from a 5/1 ARM?

While both have a 5-year fixed introductory rate, a 5/6 ARM adjusts every 6 months after the initial period, whereas a 5/1 ARM adjusts once every year.

Q4: Are there limits to how high my ARM rate can go?

Yes. ARMs include rate caps, such as initial, periodic, and lifetime caps, which strictly limit how much your interest rate can increase over the life of the loan.

Q5: Can I refinance my adjustable-rate mortgage later?

Absolutely. Many homeowners choose a rate and term refinance to switch from an ARM to a fixed-rate mortgage before their initial fixed period expires to lock in a stable rate.

Ready to explore your mortgage options in Austin?

Contact the Josh Brown Team today at 1-512-776-1413 or email us at josh@joshbrownteam.com.