The Complete Guide to an Assumable Mortgage in Austin, TX

—

What is an Assumable Mortgage and How Does It Work?

If you are navigating the dynamic Austin, TX real estate market, you have likely heard the term assumable mortgage. An assumable mortgage, also known as a mortgage assumption, is a unique financing arrangement where a homebuyer takes over the seller’s existing home loan. Instead of applying for a brand new mortgage at current market rates, the buyer assumes the remaining balance, the repayment schedule, and most importantly, the original interest rate of the seller.

In a housing market where interest rates fluctuate, finding a home with an assumable mortgage can result in significant monthly savings. However, the process involves strict lender approvals and specific eligibility requirements. Buyers must still meet credit and income standards to qualify for the mortgage assumption. Furthermore, if the home’s purchase price exceeds the remaining loan balance, the buyer will need to cover the difference in cash or secure secondary financing.

At the Josh Brown Team with Fairway Independent Mortgage Corporation, we know that exploring your home financing options can feel overwhelming. We are experts at providing second opinions on assumable mortgages to ensure you are making the most cost effective decision for your future. Sometimes, a traditional loan or a rate and term refinance later on might be a more suitable path, and we are here to help you weigh every option.

Types of Assumable Mortgages: FHA, VA, and USDA Loans

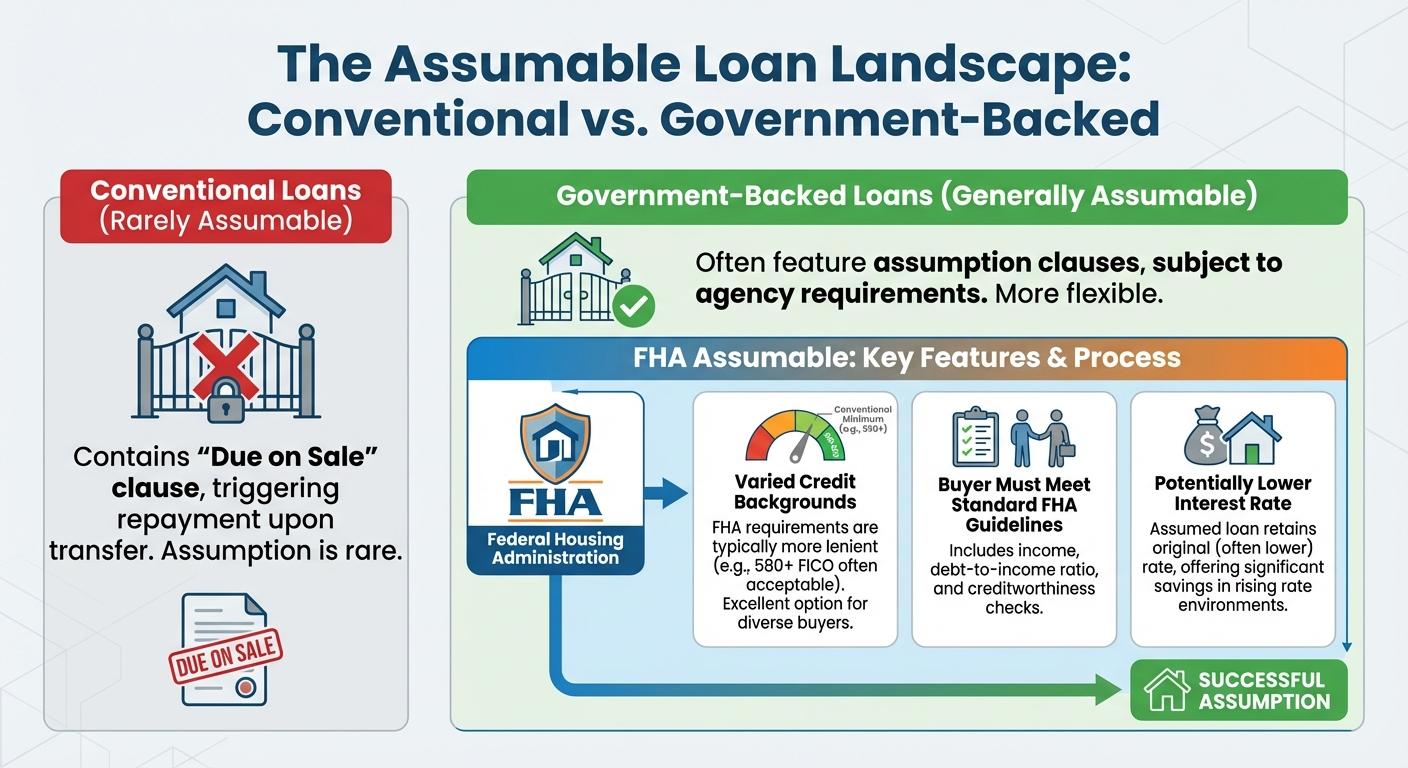

Conventional loans rarely offer assumption features because they typically contain a due on sale clause. Fortunately, government backed loans are generally assumable, provided the buyer meets the specific agency requirements. Here is a comprehensive look at the three main types of assumable loans:

- FHA Assumable: Backed by the Federal Housing Administration, an FHA assumable loan is a fantastic option for buyers with varied credit backgrounds. To assume this loan, the buyer must meet standard FHA credit and income requirements. If you are considering this route, it is also wise to compare it with a new FHA purchase loan to see which offers the best long term value.

- VA Assumable: Department of Veterans Affairs loans are highly sought after due to their favorable terms. A VA assumable loan allows a buyer to take over the veteran’s mortgage. Interestingly, the buyer does not necessarily need to be a veteran. However, if a non veteran assumes the loan, the original veteran’s VA entitlement remains tied to the property until the loan is paid off. If an eligible veteran buyer substitutes their own entitlement, the seller’s entitlement is restored. You can learn more about standard veteran financing through our VA purchase loan resources.

- USDA Assumable: Designed for rural and suburban homebuyers, USDA assumable loans allow buyers to take over mortgages on properties located in USDA eligible areas. The buyer must meet the USDA’s strict income limits and use the property as their primary residence.

| Loan Type | Assumable? | Key Requirement | Best For |

|---|---|---|---|

| FHA Loan | Yes | Lender approval & FHA credit standards | First-time buyers & moderate credit |

| VA Loan | Yes | Entitlement substitution for sellers | Veterans & active-duty military |

| USDA Loan | Yes | Property must be in an eligible rural area | Rural homebuyers with income limits |

| Conventional Loan | Rarely | Usually blocked by due-on-sale clause | Buyers needing flexible terms |

Why Get a Second Opinion on Your Mortgage Assumption?

While taking over a low interest rate sounds perfect on paper, a mortgage assumption is a complex legal and financial transaction. The process can take longer than a traditional closing, and the original lender holds the power to approve or deny your application. Additionally, you must account for the equity gap. If a home is selling for $500,000 but the assumable mortgage balance is only $350,000, you will need to bring $150,000 to the closing table or secure a second mortgage.

This is exactly why you need expert guidance. We are experts at providing second opinions on assumable mortgages. The Josh Brown Team at Fairway Independent Mortgage Corporation will review the terms of the assumption, calculate your total out of pocket costs, and compare them against current market alternatives. We proudly serve the Austin, TX community and beyond, ensuring you have clear communication and a straightforward lending process.

Before you commit to a mortgage assumption, let us run the numbers. We can help you determine if assuming a loan is truly your best financial move, or if another tailored mortgage solution fits your unique needs better.

Q1: What is an assumable mortgage?

An assumable mortgage is a home loan that allows a buyer to take over the seller’s existing mortgage. The buyer assumes the current principal balance, the repayment schedule, and the original interest rate.

Q2: Are conventional loans assumable?

In most cases, conventional loans are not assumable. They typically contain a due on sale clause that requires the mortgage to be paid in full when the property is sold. Government backed loans like FHA, VA, and USDA are the most common assumable mortgages.

Q3: Can anyone assume a VA loan?

Yes, a non veteran can assume a VA loan. However, the original veteran seller will not regain their VA loan entitlement until the assumed loan is fully paid off, unless the buyer is an eligible veteran who agrees to substitute their own entitlement.

Q4: Do I need a down payment for a mortgage assumption?

You will need to cover the difference between the home’s purchase price and the remaining balance of the assumable mortgage. This difference is known as the equity gap and must be paid in cash or financed through a second mortgage.

Q5: How long does a mortgage assumption take to process in Austin, TX?

Mortgage assumptions can take longer than traditional loan originations. Depending on the original lender’s internal processes and current volume, it can take anywhere from 45 to 90 days to finalize the assumption.

Schedule Your Free Loan Consultation with the Josh Brown Team