Your Complete Guide to Condo Mortgage Financing in Austin, TX

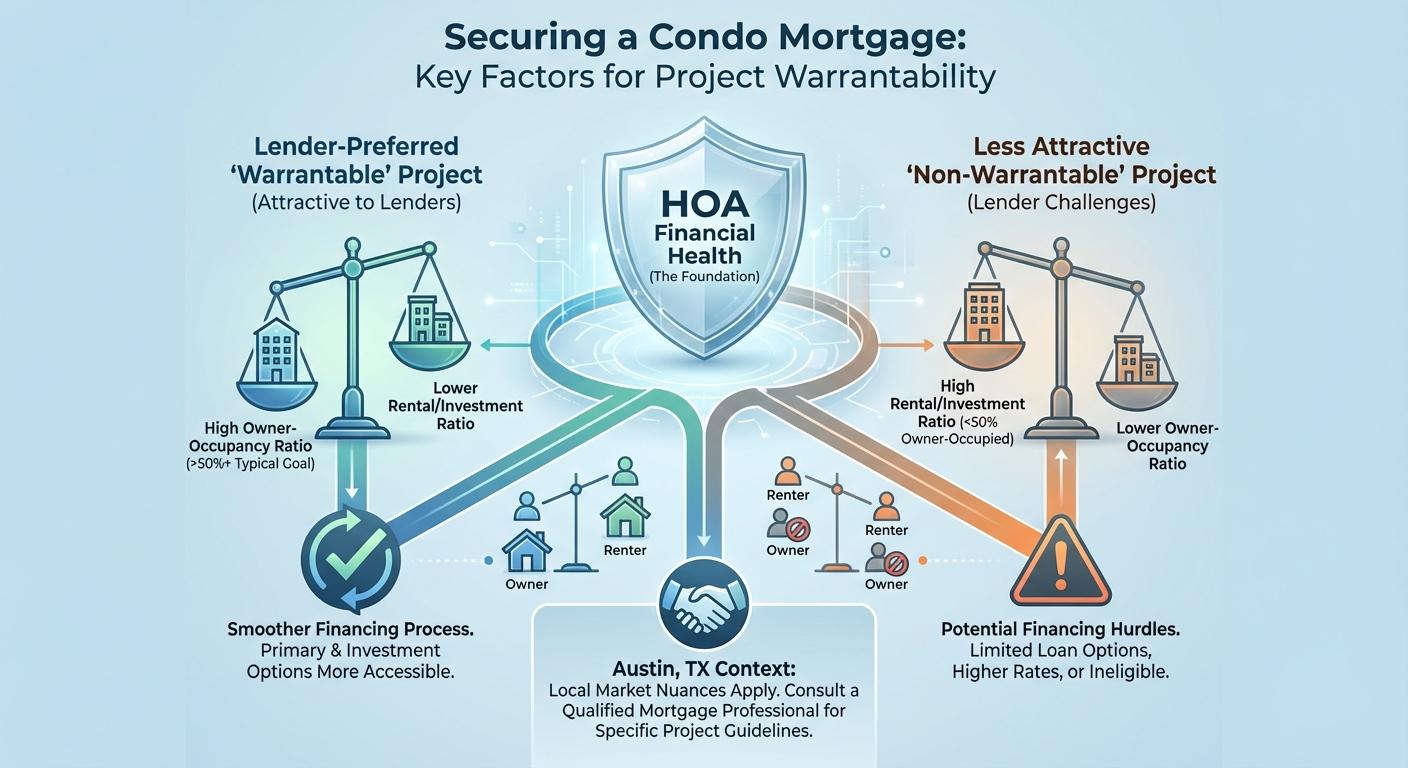

- Owner-Occupancy Ratios: Lenders prefer a high percentage of owner-occupied units compared to rentals.

- HOA Financial Health: The HOA must have adequate reserve funds for future repairs and maintenance.

- Commercial Space Restrictions: The building should not have excessive commercial space.

- Single-Entity Ownership: No single investor or entity should own more than 20% of the units in the project.

If a condo fails to meet these criteria, you will need a non-warrantable condo loan, which might come with slightly higher interest rates or require a larger down payment. The Josh Brown Team can expertly guide you through these nuances, ensuring you secure the ideal financing for your Texas property.

| Condo Feature | Warrantable Condo | Non-Warrantable Condo |

|---|---|---|

| Fannie Mae/Freddie Mac Approval | Approved and eligible | Not eligible |

| HOA Delinquency Rate | Under 15% of units | Over 15% of units |

| Commercial Space | Less than 35% | More than 35% |

| Financing Options | Conventional, FHA, VA | Specialized Portfolio Loans |

| Down Payment | As low as 3% to 5% | Typically 10% to 20% or more |

Why Choose the Josh Brown Team for Your Condo Loans?

Finding the right partner for your condo mortgage financing in Austin can make all the difference. As a branch manager and senior loan officer at Fairway Independent Mortgage Corporation, Josh Brown and his team specialize in providing tailored mortgage solutions. We do not just process loans; we educate our clients and offer transparent, professional guidance from start to finish.

Here is why Austin homebuyers trust us with their condo loans:

- Second Opinions: We are experts at providing second opinions on condo financing. If another lender has told you a project is non-warrantable or denied your application, let us take a look. We often find creative solutions others miss.

- Comprehensive Loan Options: From a standard conventional fixed-rate mortgage to specialized non-warrantable condo loans, we have a vast portfolio of products.

- Local Market Expertise: We know the Austin, TX condo market inside and out, helping you anticipate HOA document requests and project approvals quickly.

Do not let the complexities of a condo mortgage deter you from homeownership. With our dedicated team, you will enjoy a seamless, stress-free closing experience. Contact us at 15127761413 or email josh@joshbrownteam.com to get started.

Q1: What is condo mortgage financing?

Condo mortgage financing is a specialized type of home loan used to purchase a condominium. Unlike single-family homes, lenders evaluate both the borrower’s financial health and the condo project’s financial stability.

Q2: What is the difference between a warrantable and non-warrantable condo?

A warrantable condo meets the lending guidelines of Fannie Mae and Freddie Mac, making it easier to finance. A non-warrantable condo does not meet these standards due to factors like high rental ratios or HOA litigation, and it requires specialized loan products.

Q3: Can I use an FHA loan to buy a condo in Austin, TX?

Yes, you can use an FHA purchase loan to buy a condo, provided the condominium project is on the FHA-approved list or meets the requirements for a single-unit approval.

Q4: Do condo loans have higher interest rates?

Sometimes. Mortgage rates for condos can be slightly higher than for single-family homes because lenders view shared-living structures as carrying a slightly higher risk. However, a strong credit score and down payment can help secure competitive rates.

Q5: Can I get a second opinion if my condo loan was denied?

Absolutely. The Josh Brown Team are experts at providing second opinions on condo financing. We often uncover alternative financing options for complex or non-warrantable condo projects.

Schedule Your Free Condo Loan Consultation Today

- Warrantable Condos: These are condo projects that meet the strict guidelines set by government-backed entities like Fannie Mae and Freddie Mac. Because they are considered lower risk, securing a conventional fixed-rate mortgage or an FHA purchase loan for these properties is generally straightforward.

- Non-Warrantable Condos: If a condo project falls short of these guidelines, it is deemed non-warrantable. Financing these units is trickier, but certainly not impossible with the right mortgage lender.

If you have been turned down previously or simply want to ensure you are getting the best terms, we are experts at providing second opinions on condo financing. Our goal is clear communication and a straightforward lending process tailored to your unique needs.

Key Factors Lenders Look For in a Condo Project

To ensure a smooth condo mortgage financing process, it is essential to understand what makes a condo project attractive to lenders. Whether you are buying your primary residence or seeking an investment property mortgage, the financial health of the Homeowners Association (HOA) plays a massive role.

Here are a few key factors that typically determine if an Austin, TX condo is warrantable:

- Owner-Occupancy Ratios: Lenders prefer a high percentage of owner-occupied units compared to rentals.

- HOA Financial Health: The HOA must have adequate reserve funds for future repairs and maintenance.

- Commercial Space Restrictions: The building should not have excessive commercial space.

- Single-Entity Ownership: No single investor or entity should own more than 20% of the units in the project.

If a condo fails to meet these criteria, you will need a non-warrantable condo loan, which might come with slightly higher interest rates or require a larger down payment. The Josh Brown Team can expertly guide you through these nuances, ensuring you secure the ideal financing for your Texas property.

| Condo Feature | Warrantable Condo | Non-Warrantable Condo |

|---|---|---|

| Fannie Mae/Freddie Mac Approval | Approved and eligible | Not eligible |

| HOA Delinquency Rate | Under 15% of units | Over 15% of units |

| Commercial Space | Less than 35% | More than 35% |

| Financing Options | Conventional, FHA, VA | Specialized Portfolio Loans |

| Down Payment | As low as 3% to 5% | Typically 10% to 20% or more |

Why Choose the Josh Brown Team for Your Condo Loans?

Finding the right partner for your condo mortgage financing in Austin can make all the difference. As a branch manager and senior loan officer at Fairway Independent Mortgage Corporation, Josh Brown and his team specialize in providing tailored mortgage solutions. We do not just process loans; we educate our clients and offer transparent, professional guidance from start to finish.

Here is why Austin homebuyers trust us with their condo loans:

- Second Opinions: We are experts at providing second opinions on condo financing. If another lender has told you a project is non-warrantable or denied your application, let us take a look. We often find creative solutions others miss.

- Comprehensive Loan Options: From a standard conventional fixed-rate mortgage to specialized non-warrantable condo loans, we have a vast portfolio of products.

- Local Market Expertise: We know the Austin, TX condo market inside and out, helping you anticipate HOA document requests and project approvals quickly.

Do not let the complexities of a condo mortgage deter you from homeownership. With our dedicated team, you will enjoy a seamless, stress-free closing experience. Contact us at 15127761413 or email josh@joshbrownteam.com to get started.

Q1: What is condo mortgage financing?

Condo mortgage financing is a specialized type of home loan used to purchase a condominium. Unlike single-family homes, lenders evaluate both the borrower’s financial health and the condo project’s financial stability.

Q2: What is the difference between a warrantable and non-warrantable condo?

A warrantable condo meets the lending guidelines of Fannie Mae and Freddie Mac, making it easier to finance. A non-warrantable condo does not meet these standards due to factors like high rental ratios or HOA litigation, and it requires specialized loan products.

Q3: Can I use an FHA loan to buy a condo in Austin, TX?

Yes, you can use an FHA purchase loan to buy a condo, provided the condominium project is on the FHA-approved list or meets the requirements for a single-unit approval.

Q4: Do condo loans have higher interest rates?

Sometimes. Mortgage rates for condos can be slightly higher than for single-family homes because lenders view shared-living structures as carrying a slightly higher risk. However, a strong credit score and down payment can help secure competitive rates.

Q5: Can I get a second opinion if my condo loan was denied?

Absolutely. The Josh Brown Team are experts at providing second opinions on condo financing. We often uncover alternative financing options for complex or non-warrantable condo projects.

Schedule Your Free Condo Loan Consultation Today

—

Understanding Condo Financing: Warrantable vs. Non-Warrantable Condos

Navigating the world of condo mortgage financing in Austin, TX, can feel a bit different than buying a traditional single-family home. Whether you are looking for a sleek downtown high-rise or a cozy suburban community, securing the right condo loans requires a specialized approach. At the Josh Brown Team, we bring over 25 years of expertise to help you make informed and confident home financing decisions.

When you apply for a condo mortgage, lenders do not just evaluate your financial profile; they also evaluate the condominium project itself. This brings us to two critical terms you will encounter: warrantable and non-warrantable condos.

- Warrantable Condos: These are condo projects that meet the strict guidelines set by government-backed entities like Fannie Mae and Freddie Mac. Because they are considered lower risk, securing a conventional fixed-rate mortgage or an FHA purchase loan for these properties is generally straightforward.

- Non-Warrantable Condos: If a condo project falls short of these guidelines, it is deemed non-warrantable. Financing these units is trickier, but certainly not impossible with the right mortgage lender.

If you have been turned down previously or simply want to ensure you are getting the best terms, we are experts at providing second opinions on condo financing. Our goal is clear communication and a straightforward lending process tailored to your unique needs.

Key Factors Lenders Look For in a Condo Project

To ensure a smooth condo mortgage financing process, it is essential to understand what makes a condo project attractive to lenders. Whether you are buying your primary residence or seeking an investment property mortgage, the financial health of the Homeowners Association (HOA) plays a massive role.

Here are a few key factors that typically determine if an Austin, TX condo is warrantable:

- Owner-Occupancy Ratios: Lenders prefer a high percentage of owner-occupied units compared to rentals.

- HOA Financial Health: The HOA must have adequate reserve funds for future repairs and maintenance.

- Commercial Space Restrictions: The building should not have excessive commercial space.

- Single-Entity Ownership: No single investor or entity should own more than 20% of the units in the project.

If a condo fails to meet these criteria, you will need a non-warrantable condo loan, which might come with slightly higher interest rates or require a larger down payment. The Josh Brown Team can expertly guide you through these nuances, ensuring you secure the ideal financing for your Texas property.

| Condo Feature | Warrantable Condo | Non-Warrantable Condo |

|---|---|---|

| Fannie Mae/Freddie Mac Approval | Approved and eligible | Not eligible |

| HOA Delinquency Rate | Under 15% of units | Over 15% of units |

| Commercial Space | Less than 35% | More than 35% |

| Financing Options | Conventional, FHA, VA | Specialized Portfolio Loans |

| Down Payment | As low as 3% to 5% | Typically 10% to 20% or more |

Why Choose the Josh Brown Team for Your Condo Loans?

Finding the right partner for your condo mortgage financing in Austin can make all the difference. As a branch manager and senior loan officer at Fairway Independent Mortgage Corporation, Josh Brown and his team specialize in providing tailored mortgage solutions. We do not just process loans; we educate our clients and offer transparent, professional guidance from start to finish.

Here is why Austin homebuyers trust us with their condo loans:

- Second Opinions: We are experts at providing second opinions on condo financing. If another lender has told you a project is non-warrantable or denied your application, let us take a look. We often find creative solutions others miss.

- Comprehensive Loan Options: From a standard conventional fixed-rate mortgage to specialized non-warrantable condo loans, we have a vast portfolio of products.

- Local Market Expertise: We know the Austin, TX condo market inside and out, helping you anticipate HOA document requests and project approvals quickly.

Do not let the complexities of a condo mortgage deter you from homeownership. With our dedicated team, you will enjoy a seamless, stress-free closing experience. Contact us at 15127761413 or email josh@joshbrownteam.com to get started.

Q1: What is condo mortgage financing?

Condo mortgage financing is a specialized type of home loan used to purchase a condominium. Unlike single-family homes, lenders evaluate both the borrower’s financial health and the condo project’s financial stability.

Q2: What is the difference between a warrantable and non-warrantable condo?

A warrantable condo meets the lending guidelines of Fannie Mae and Freddie Mac, making it easier to finance. A non-warrantable condo does not meet these standards due to factors like high rental ratios or HOA litigation, and it requires specialized loan products.

Q3: Can I use an FHA loan to buy a condo in Austin, TX?

Yes, you can use an FHA purchase loan to buy a condo, provided the condominium project is on the FHA-approved list or meets the requirements for a single-unit approval.

Q4: Do condo loans have higher interest rates?

Sometimes. Mortgage rates for condos can be slightly higher than for single-family homes because lenders view shared-living structures as carrying a slightly higher risk. However, a strong credit score and down payment can help secure competitive rates.

Q5: Can I get a second opinion if my condo loan was denied?

Absolutely. The Josh Brown Team are experts at providing second opinions on condo financing. We often uncover alternative financing options for complex or non-warrantable condo projects.