Your Guide to a Conventional Fixed-Rate Mortgage in Austin, TX

—

Your Guide to a Conventional Fixed-Rate Mortgage in Austin, TX

Understanding the Basics of a Conventional Mortgage

If you are looking to buy a home in Austin, Texas, a conventional mortgage is one of the most popular and flexible financing options available. A conventional fixed-rate mortgage provides the stability of a set interest rate and predictable monthly payments for the life of your loan. Unlike government-backed options like an FHA purchase loan, conventional loans are not insured by the federal government. Instead, they are backed by private lenders and often follow guidelines set by Fannie Mae and Freddie Mac.

At the Josh Brown Team, we know that navigating the Austin real estate market requires expert guidance. Whether you are a first-time homebuyer or looking to upgrade, understanding your loan options is crucial. Many buyers prefer the classic 30-year fixed-rate mortgage because it spreads payments out over three decades, making homeownership more affordable. If you already have a quote from another lender, we are experts at providing second opinions on conventional mortgages to ensure you are getting the best possible terms and rates.

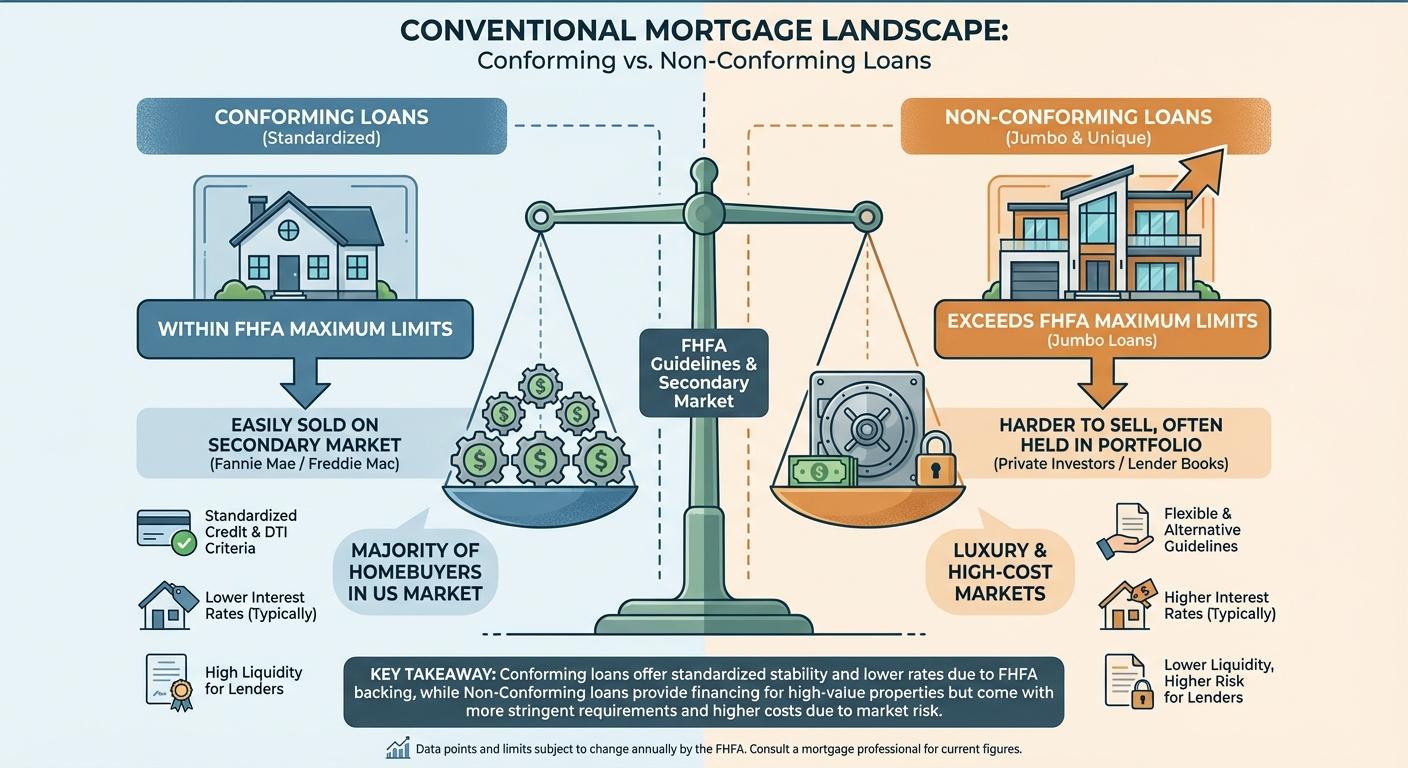

Conforming vs. Non-Conforming Conventional Loans

When diving into the world of a conventional mortgage, it is essential to understand the difference between conforming and non-conforming loans. This distinction primarily comes down to the loan amount and the specific guidelines set by the Federal Housing Finance Agency (FHFA).

- Conforming Loans: These loans fall within the maximum loan limits established by the FHFA. Because they meet these standardized guidelines, lenders can easily sell them on the secondary market. For most homebuyers in Austin, a conforming conventional fixed-rate mortgage offers highly competitive interest rates and favorable terms.

- Non-Conforming Loans: If a loan exceeds the FHFA limits or does not meet other specific criteria, it is considered non-conforming. The most common type of non-conforming loan is a jumbo mortgage. Austin has many luxury properties and high-value neighborhoods where a jumbo loan is the perfect financing solution.

Choosing between a conforming and non-conforming conventional mortgage depends entirely on your target property and financial profile. The Josh Brown Team can help you evaluate your income, credit score, and down payment capabilities to find the exact fit for your home financing journey.

| Feature | Conforming Conventional Mortgage | Non-Conforming (Jumbo) Mortgage |

|---|---|---|

| Loan Limits | Adheres to annual FHFA loan limits | Exceeds FHFA loan limits |

| Credit Score Requirement | Typically 620 or higher | Usually requires a stricter 700+ score |

| Down Payment | As low as 3% for qualified buyers | Often requires 10% to 20% or more |

| Interest Rates | Highly competitive standard rates | Can be slightly higher due to lender risk |

Why Choose the Josh Brown Team for Your Conventional Mortgage

Securing a conventional fixed-rate mortgage is a major financial milestone, and you deserve a lending partner who prioritizes your goals. With over 25 years of experience, Josh Brown and his team at Fairway Independent Mortgage Corporation provide mortgage solutions designed to support informed and confident home financing decisions.

We pride ourselves on clear communication, education, and a straightforward lending process. If you are currently shopping for a home in Austin, TX, or looking to refinance an existing loan, we encourage you to reach out. Remember, we are experts at providing second opinions on conventional mortgages. A quick review of your current loan estimate could potentially save you thousands of dollars over the life of your loan. Let us guide you every step of the way toward securing the home of your dreams.

Q1: What is a conventional fixed-rate mortgage?

A conventional fixed-rate mortgage is a home loan not backed by a government agency, featuring an interest rate that remains exactly the same for the entire duration of the loan.

Q2: What credit score do I need for a conventional mortgage in Austin?

Generally, you need a minimum credit score of 620 to qualify for a conventional mortgage, though higher scores often unlock the most competitive interest rates.

Q3: How much of a down payment is required?

While many believe you need a 20 percent down payment, qualified first-time homebuyers can secure a conventional mortgage with as little as 3 percent down.

Q4: Can I get a second opinion on my conventional mortgage offer?

Absolutely. The Josh Brown Team specializes in providing expert second opinions to ensure you receive the best rates and terms available for your unique financial situation.

Q5: Do I have to pay mortgage insurance on a conventional loan?

If your down payment is less than 20 percent, you will typically need to pay Private Mortgage Insurance (PMI). However, PMI can be canceled once you build sufficient equity in your home.