The Ultimate Guide to Cash-Out Refinance in Austin, TX

What is a Cash-Out Refinance and How Can It Benefit You?

If you are a homeowner in Austin, TX, you might be sitting on a significant amount of home equity. A cash out refinance, sometimes referred to as a cash-out mortgage, allows you to tap into that equity by replacing your current mortgage with a new, larger loan. You receive the difference in cash, which you can use for home improvements, investments, or securing a debt consolidation mortgage.

Unlike a rate and term refinance where you simply adjust your interest rate or loan duration, a cash out refinance puts liquid funds directly into your hands. At the Josh Brown Team, we are experts at providing second opinions on cash-out refinance options, ensuring you get the best possible terms for your financial goals.

Exploring Your Cash-Out Mortgage Options: Conventional, FHA, and VA

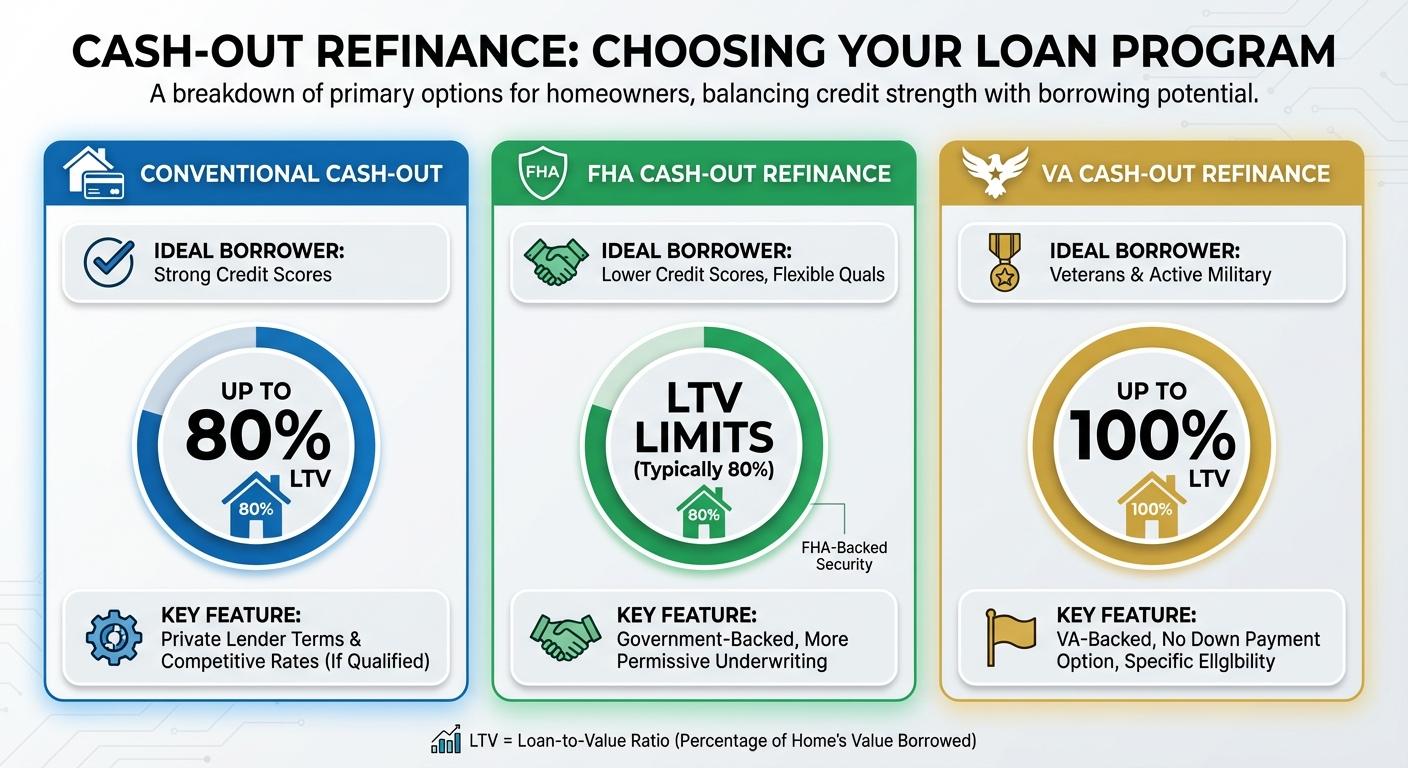

Choosing the right loan program is critical when planning a cash out refinance. Here is a breakdown of the primary options available to homeowners:

- Conventional Cash-Out Refinance: Ideal for borrowers with strong credit scores. This option typically allows you to borrow up to 80 percent of your home’s value.

- FHA Cash-Out Refinance: A great choice if your credit score is lower. Backed by the Federal Housing Administration, this loan offers flexible qualification requirements.

- VA Cash-Out Refinance: Available exclusively to eligible veterans and active-duty military. We specialize in VA loans and can help you leverage this incredible benefit, which often allows you to finance up to 100 percent of your home’s value.

If you are unsure whether a new primary mortgage is right for you, we can also help you explore alternatives like a home equity line of credit HELOC. Getting a second opinion from our Austin based experts ensures you have all the facts before making a decision.

| Loan Type | Maximum Loan-to-Value (LTV) | Minimum Credit Score (Typical) | Best For |

|---|---|---|---|

| Conventional | 80% | 620 | Homeowners with strong credit and high equity |

| FHA | 80% | 580 | Borrowers needing flexible credit requirements |

| VA | Up to 100% | 580 to 620 | Eligible Veterans and active-duty military |

Why Choose the Josh Brown Team for Your Cash-Out Refinance?

Navigating the mortgage process requires a trusted partner. The Josh Brown Team with Fairway Independent Mortgage Corporation provides mortgage solutions designed to support informed and confident home financing decisions. With over 25 years of experience, Branch Manager Josh Brown (NMLS: 216153) and his team focus on clear communication, education, and a straightforward lending process.

We highly recommend getting a second opinion on your cash out refinance. Many lenders offer standard rates, but our deep understanding of the Austin real estate market allows us to tailor a solution specific to your needs. Whether you want to remodel your home or consolidate high-interest debt, our personalized service ensures your financial health remains the top priority. Fairway Independent Mortgage Corporation NMLS: 2289. Equal Housing Opportunity.

Q1: What is a cash out refinance?

A cash out refinance replaces your existing mortgage with a new loan for more than you owe. You receive the difference in cash, which can be used for various financial needs.

Q2: How long does a cash out refinance take to close?

Typically, the process takes between 30 to 45 days, depending on how quickly you provide documentation and the current appraisal turnaround times in Austin, TX.

Q3: Can I get a cash out refinance with a VA loan?

Yes, eligible veterans can utilize a VA cash out refinance, which often allows you to borrow up to 100 percent of your home’s appraised value.

Q4: Is it better to get a cash out refinance or a HELOC?

It depends on your current interest rate and financial goals. A cash out refinance gives you a lump sum with a fixed rate, while a home equity line of credit HELOC acts as a revolving line of credit. We offer second opinions to help you decide.

Q5: Can I use a cash out refinance to pay off credit card debt?

Absolutely. Many homeowners use the funds for a debt consolidation mortgage strategy, paying off high-interest credit cards with the lower interest rate of a mortgage.