Your Guide to Navigating a First-Time Homebuyer Mortgage in Austin, TX

Understanding First-Time Buyer Loans and Programs

Buying your very first home in Austin, TX, is an exciting milestone, but the financing process can feel overwhelming. Securing the right first time homebuyer mortgage is crucial to ensuring your monthly payments fit comfortably into your lifestyle. At the Josh Brown Team with Fairway Independent Mortgage Corporation, we specialize in helping Austin residents navigate their First-Time Buyer Loans with confidence and clarity.

Whether you are just starting to explore options or you already have a quote, we are experts at providing second opinions on first-time homebuyer mortgages. A second look can often reveal better rates or more suitable loan structures that save you thousands over the life of your loan.

Two of the most popular conventional options for a First-Time Home Buyer Mortgage are the Fannie Mae HomeReady and Freddie Mac Home Possible programs. Both are designed to help buyers with moderate incomes achieve homeownership with lower down payments and flexible credit requirements. If you are exploring all your options, you might also want to look into an FHA purchase loan, which is another excellent government-backed choice, or explore local down payment assistance programs to help cover upfront costs.

HomeReady vs. Home Possible: Which is Right for You?

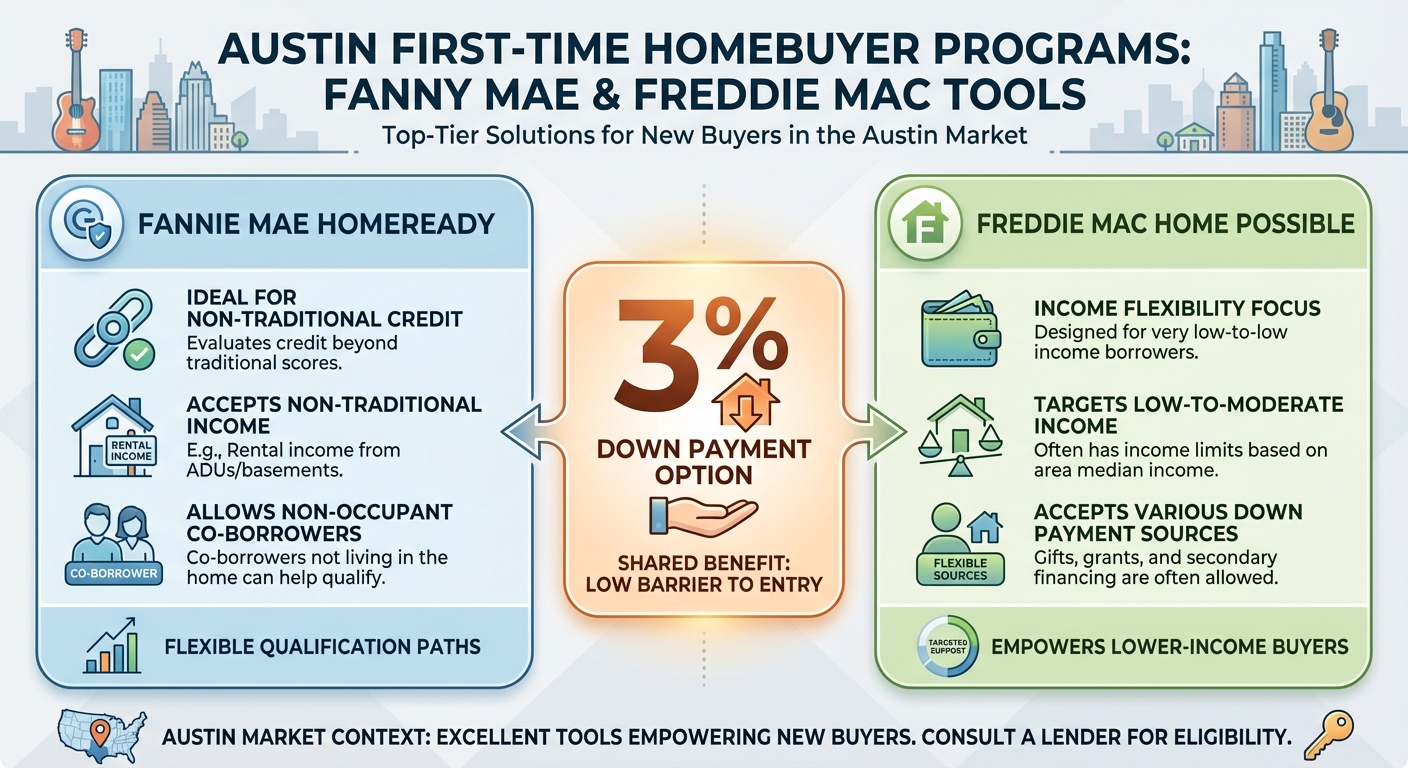

When comparing top tier first time homebuyer mortgage programs, Fannie Mae’s HomeReady and Freddie Mac’s Home Possible stand out as excellent tools for new buyers in the Austin market.

- Fannie Mae HomeReady: This program allows for a down payment as low as 3%. It is ideal for buyers who might have non-traditional credit or income sources, such as rental income from a basement apartment or co-borrowers who will not live in the home.

- Freddie Mac Home Possible: Also offering a 3% down payment option, this program is geared toward very low to low-income borrowers. It provides flexibility with credit scores and offers reduced mortgage insurance premiums, making your monthly payments more manageable.

Both programs require you to complete a homeownership education course, which is an invaluable resource for anyone taking out a first time home buyer mortgage. By understanding the nuances of these First-Time Buyer Loans, you can make an informed decision that aligns with your financial goals in Texas.

| Feature | Fannie Mae HomeReady | Freddie Mac Home Possible |

|---|---|---|

| Minimum Down Payment | 3% | 3% |

| Minimum Credit Score | Typically 620 | Typically 660 |

| Income Limits | Up to 80% of Area Median Income (AMI) | Up to 80% of Area Median Income (AMI) |

| Mortgage Insurance | Reduced rates; cancelable at 20% equity | Reduced rates; cancelable at 20% equity |

| Homebuyer Education | Required for at least one borrower | Required for at least one borrower |

Why Get a Second Opinion on Your Mortgage?

Many buyers accept the very first loan estimate they receive, unaware that mortgage terms can vary significantly between lenders. Because we are experts at providing second opinions on first-time homebuyer mortgages, we highly encourage Austin buyers to let us review their initial offers.

Our team will carefully analyze your current quote and compare it against a wide range of First-Time Buyer Loans. We look at the interest rate, lender fees, and long-term costs. Sometimes, switching from a conventional loan to an FHA purchase loan or utilizing down payment assistance programs can drastically improve your financial outlook. At the Josh Brown Team, transparency is our priority, and we will always give you honest advice on whether your current offer is truly the best fit for your home financing journey.

Q1: What qualifies me for a first time homebuyer mortgage in Austin, TX?

Generally, you are considered a first-time homebuyer if you have not owned a principal residence in the past three years. You will need to meet specific credit score, income, and debt-to-income ratio requirements depending on the loan program.

Q2: Can I buy a home with no down payment?

Yes, certain programs like VA loans or USDA loans offer zero down payment options. Additionally, utilizing down payment assistance programs can help cover the upfront costs of a HomeReady or Home Possible loan.

Q3: What is the difference between an FHA loan and a conventional first-time buyer loan?

An FHA loan is backed by the government and typically allows for lower credit scores, while conventional loans like HomeReady are backed by private lenders and may offer lower mortgage insurance costs for borrowers with good credit.

Q4: Why should I get a second opinion on my mortgage offer?

Mortgage rates and fees vary by lender. As experts in providing second opinions on first-time homebuyer mortgages, we can review your offer to ensure you are getting the most competitive rate and lowest fees available.

Q5: Do I have to take a homebuyer education course?

For specific programs like HomeReady and Home Possible, at least one borrower is required to complete a certified homeownership education course. This helps ensure you are fully prepared for the responsibilities of owning a home.