The Ultimate Guide to the FHA 203(k) Renovation Loan in Austin, TX

What is an FHA 203k Loan and How Does It Work?

If you are looking to buy a fixer-upper in Austin, TX, or want to upgrade your current home, an FHA 203k loan might be the perfect financing solution. Also known as an FHA 203(k) Renovation Loan, this unique mortgage allows you to finance both the purchase or refinance of a house and the cost of its rehabilitation through a single mortgage.

At the Josh Brown Team, we understand that navigating the real estate market in Austin can be highly competitive. Finding a move-in ready home within your budget is not always easy. That is where the FHA 203k loan comes in. It empowers you to buy a property that needs a little TLC and transform it into your dream home. Because these loans are backed by the Federal Housing Administration, they come with flexible credit requirements and low down payment options, similar to a standard FHA purchase loan.

As trusted local mortgage lenders, we are also experts at providing second opinions on FHA 203k renovation loans. If you have been told a project cannot be done or you simply want to ensure you are getting the best terms, our team is here to help you review your options.

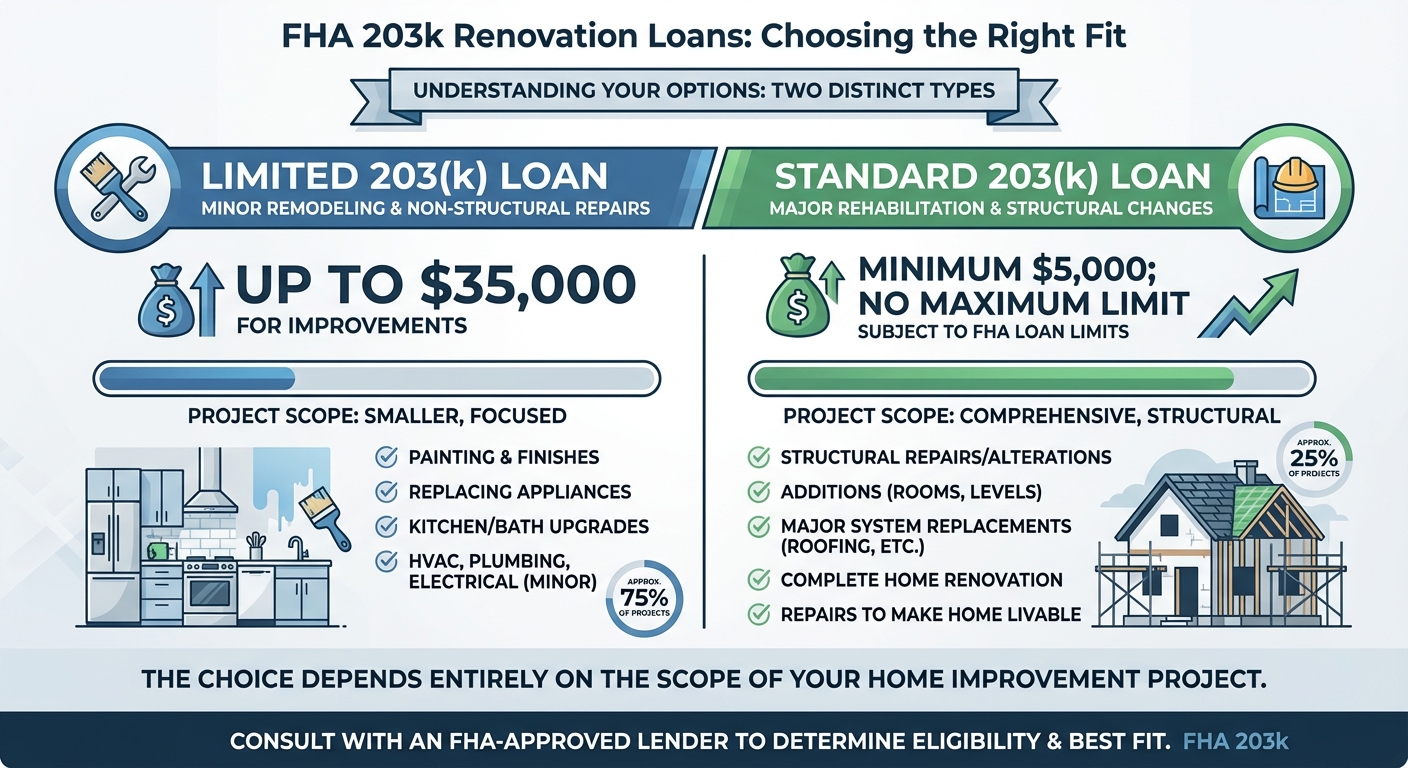

Standard 203(k) vs. Limited 203(k): Which is Right for You?

When exploring an FHA 203k renovation loan, it is crucial to understand that there are two distinct types available to borrowers: the Standard 203(k) and the Limited 203(k). Choosing the right one depends entirely on the scope of your home improvement project.

- Limited 203(k) Loan: This option is designed for minor remodeling and non-structural repairs. It allows you to finance up to $35,000 into your mortgage for improvements like painting, replacing appliances, or upgrading a kitchen. It is a streamlined process that does not require a HUD consultant.

- Standard 203(k) Loan: If your Austin property requires structural changes, room additions, or major landscaping, the Standard 203(k) is the way to go. There is no strict cap on the repair costs, provided the total loan amount falls within FHA loan limits for Travis County. This version requires a HUD consultant to oversee the architectural plans and construction process.

If you are considering non-FHA options, you might also want to compare these features with a conventional renovation loan to see which aligns best with your financial goals.

| Feature | Limited 203(k) Loan | Standard 203(k) Loan |

|---|---|---|

| Best For | Cosmetic upgrades, minor repairs | Major renovations, structural changes |

| Repair Cost Limit | Up to $35,000 | No limit (subject to max FHA loan limits) |

| Minimum Repair Cost | None | $5,000 |

| Structural Repairs Allowed? | No | Yes |

| HUD Consultant Required? | No | Yes |

Why Choose the Josh Brown Team for Your Austin Renovation Loan?

Securing an FHA 203k loan requires a lender with specific expertise. The paperwork, contractor approvals, and appraisal processes are more complex than a standard mortgage. At the Josh Brown Team with Fairway Independent Mortgage Corporation, we pride ourselves on clear communication and a straightforward lending process tailored for the Austin, TX market.

We have over 25 years of experience providing tailored mortgage solutions. Whether you are buying a historic home in Hyde Park or updating a mid-century property in South Austin, we guide you through every step. Remember, we are experts at providing second opinions on FHA 203k renovation loans. If you hit a roadblock with another lender, reach out to us. We will thoroughly review your file and help you get your renovation project back on track.

Q1: What credit score do I need for an FHA 203k loan?

Generally, you need a minimum credit score of 580 to qualify for the maximum financing of 96.5%. However, lender overlays may apply, so it is best to consult with the Josh Brown Team to review your specific financial situation.

Q2: Can I do the renovation work myself with an FHA 203k loan?

FHA guidelines typically require that all renovation work be completed by licensed and insured contractors. Self-help or DIY repairs are rarely approved unless you can prove you are a licensed professional in that specific trade.

Q3: Can I use an FHA 203k loan for an investment property?

No, FHA 203k loans are exclusively for primary residences. You must intend to live in the home once the renovations are complete. However, you can use it to purchase a multi-unit property (up to 4 units) as long as you occupy one of the units.

Q4: How long do I have to complete the repairs?

Renovations must begin within 30 days of closing, and the work must be completed within six months. Your contractor needs to adhere to a strict timeline to ensure the funds are disbursed properly.

Q5: Does the Josh Brown Team offer second opinions on renovation loans?

Yes! We are experts at providing second opinions on FHA 203k renovation loans. If another lender has denied your project or you are unsure about the terms you were offered, contact us for a comprehensive review.

Call (512) 776-1413 to Schedule Your Free FHA 203k Loan Consultation