Can I Buy a Home with No Down Payment? A Guide for Austin Buyers

For many aspiring homeowners in Austin and throughout Texas, the biggest hurdle standing between them and the keys to a new house isn’t the monthly mortgage payment—it’s the down payment. The old adage that you need to save 20% of the home’s purchase price before buying is a myth that continues to discourage credit-worthy renters from entering the market.

So, the burning question remains: Can I buy a home with no down payment?

The short answer is yes. While 20% down helps avoid Private Mortgage Insurance (PMI), there are specific government-backed loan programs and local Texas assistance options designed to help you buy a home with zero down or very low out-of-pocket costs. As a Senior Mortgage Banker at Fairway Independent Mortgage Corporation, I have helped countless families in the Austin area navigate these options to stop renting and start building equity.

In this comprehensive guide, we will explore the reality of zero down mortgages, low down payment alternatives, and specific strategies for the Central Texas housing market.

The Reality of Zero Down Mortgages

A “zero down” mortgage allows you to finance 100% of the home’s purchase price. This means you do not need to provide a lump sum for the down payment at closing. However, it is crucial to understand that “no down payment” does not mean “no cost.” You will still likely be responsible for closing costs (unless negotiated to be paid by the seller or rolled into the loan in specific scenarios) and earnest money.

Currently, the two primary standard mortgage programs that offer true 100% financing are VA Loans and USDA Loans. If you do not qualify for these, there are Down Payment Assistance (DPA) programs available specifically for Texas residents.

Top No Down Payment Loan Options

1. VA Loans (The Gold Standard for Veterans)

If you are an active-duty service member, a veteran, or a qualifying surviving spouse, the VA Loan is arguably the best mortgage product available on the market today. Backed by the Department of Veterans Affairs, this loan is designed to make homeownership affordable for those who have served our country.

Key Benefits of VA Loans:

- 0% Down Payment: You can finance 100% of the home price.

- No Private Mortgage Insurance (PMI): unlike FHA or conventional loans with low down payments, VA loans never require monthly PMI, saving you hundreds of dollars a month.

- Competitive Interest Rates: VA rates are typically lower than conventional rates.

- Flexible Credit Requirements: The VA is more forgiving regarding credit history than conventional lenders.

In the competitive Austin real estate market, having a VA loan is a powerful tool. If you believe you might be eligible, obtaining your Certificate of Eligibility (COE) is the first step.

2. USDA Loans (Rural Development Loans)

The United States Department of Agriculture (USDA) offers a zero-down mortgage program designed to encourage development in rural and suburban areas. Many buyers in the Austin area assume “rural” means farmland, but you might be surprised by the eligibility map.

Where can you use a USDA Loan near Austin?

As Austin expands, the eligible boundaries shift, but many areas on the outskirts of Travis, Williamson, and Hays counties often qualify. Towns that have historically had USDA-eligible areas include parts of Manor, Kyle, Buda, Liberty Hill, and Elgin. It is essential to check the specific property address for eligibility.

USDA Loan Requirements:

- Location: The home must be in a USDA-designated rural area.

- Income Limits: There are household income caps (115% of the area median income). This program is designed for low-to-moderate-income households.

- Primary Residence: You must occupy the home; it cannot be an investment property.

If you are willing to commute slightly to get more house for your money, a USDA loan is a fantastic way to buy with no money down.

Low Down Payment Alternatives (3% – 3.5%)

If you do not qualify for VA or USDA loans, you are not forced to save 20%. The vast majority of first-time homebuyers in Texas utilize low down payment conventional or government-insured loans.

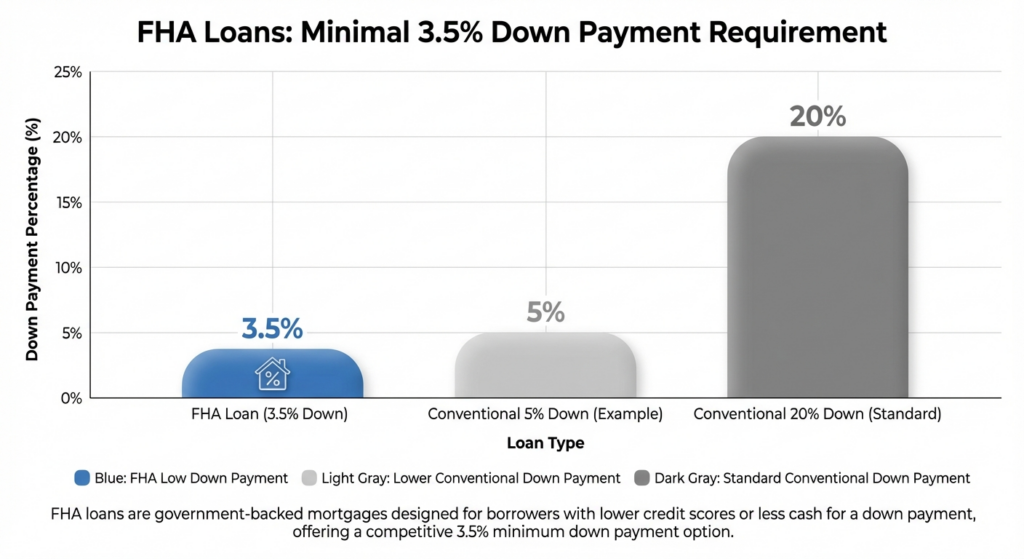

FHA Loans (3.5% Down)

The FHA Loan, backed by the Federal Housing Administration, is one of the most popular options for first-time buyers. It requires a minimum down payment of just 3.5%.

Example: On a $400,000 home in Austin, a 3.5% down payment is $14,000. While not zero, this is significantly more achievable than the $80,000 required for a 20% down payment.

- Credit Score: FHA loans are known for lenient credit score requirements, often allowing scores as low as 580 to qualify for the 3.5% down option.

- DTI Ratio: Allows for higher debt-to-income ratios than conventional loans.

Conventional 97 (3% Down)

For borrowers with stronger credit (typically 620+), a Conventional 97 loan allows for a down payment as low as 3%. This is often preferred over FHA because the Private Mortgage Insurance (PMI) can eventually be removed once you reach 20% equity, whereas FHA mortgage insurance typically stays for the life of the loan.

Texas Down Payment Assistance (DPA) Programs

What if you want an FHA or Conventional loan but don’t have the 3% or 3.5% saved? This is where Down Payment Assistance (DPA) comes into play.

In Texas, organizations like the Texas State Affordable Housing Corporation (TSAHC) and the Texas Department of Housing and Community Affairs (TDHCA) offer programs that provide grants or second liens (loans) to cover your down payment and closing costs.

How DPA Works:

- Grants: Money given to you for the down payment that does not need to be repaid.

- Forgivable Second Liens: A 0% interest loan for the down payment that is forgiven after you live in the home for a set period (e.g., 3 years).

- Repayable Second Liens: A loan for the down payment that you pay back over time.

These programs effectively allow you to buy a home with zero money out of pocket for the down payment, bridging the gap for teachers, police officers, firefighters, and low-to-moderate-income buyers in Austin.

Comparison: Loan Options at a Glance

Choosing the right loan program depends on your military status, location preference, and credit profile. Here is a quick comparison to help you visualize your options.

| Loan Type | Min. Down Payment | PMI Required? | Ideal For |

|---|---|---|---|

| VA Loan | 0% | No | Veterans & Active Military |

| USDA Loan | 0% | No (Guarantee Fee applies) | Rural/Suburban Buyers |

| FHA Loan | 3.5% | Yes (MIP) | Lower Credit Scores |

| Conventional 97 | 3% | Yes (Removable) | Good Credit First-Time Buyers |

| TSAHC / DPA | 0% (via assistance) | Yes | Buyers needing cash assistance |

Expert Insight: The Cost of Waiting

As I often tell my clients, “Time in the market beats timing the market.”

By utilizing a low or no down payment loan now, you lock in the home price and start building equity immediately. With interest rates fluctuating, getting into a home sooner allows you to refinance later if rates drop, but you cannot renegotiate the purchase price of a home once values go up.

If you are worried about monthly payments, use our Mortgage Calculator to see how different down payment amounts actually impact your monthly budget. You might find that the difference between 3.5% down and 20% down is less drastic on a monthly basis than you expect.

Steps to Qualify in Austin, TX

Ready to move forward? Here is a checklist to prepare for your zero or low down payment mortgage application:

- Check Your Credit: While FHA allows scores down to 580, higher scores (620-640+) open up DPA and USDA options.

- Stabilize Your Income: Lenders look for a two-year work history. Gaps in employment should be explained.

- Manage Your Debt: Your Debt-to-Income (DTI) ratio matters. Avoid taking out new car loans or running up credit cards before applying.

- Get Pre-Approved: A pre-qualification is an estimate, but a Pre-Approval from the Josh Brown Team proves to sellers that you are a serious buyer with financing secured.

Frequently Asked Questions (FAQs)

1. Do I need perfect credit for a zero down payment loan?

No, you do not need perfect credit. VA loans and USDA loans generally look for a credit score of 620 or higher, though exceptions exist. FHA loans allow for scores as low as 580 with a 3.5% down payment. If your score is lower, reach out to us; we can often provide guidance on how to improve it quickly.

2. Are closing costs included in “No Down Payment”?

Generally, no. The down payment is your equity contribution, while closing costs are fees for processing the loan, title work, and taxes. However, with a VA loan or by using seller concessions (where the seller agrees to pay your closing costs), it is possible to come to the closing table with almost $0 out of pocket.

3. Can I use a zero down loan for an investment property?

No. VA, USDA, and most Down Payment Assistance programs are strictly for primary residences. You must intend to live in the home. If you are looking for investment loans, standard conventional financing typically requires 15-25% down.

4. Is Private Mortgage Insurance (PMI) bad?

PMI gets a bad reputation, but it is actually a tool that allows you to buy a home sooner. Without PMI, lenders wouldn’t offer loans with less than 20% down. Think of PMI as the cost of buying a home today rather than waiting 5 years to save up. Unlike FHA loans, PMI on conventional loans falls off automatically once you reach 22% equity.

5. How do I know if a home in Austin is USDA eligible?

Eligibility is based on the property’s specific address. Areas like downtown Austin or The Domain are ineligible. However, surrounding communities are often eligible. The best way to know for sure is to contact our team, and we can run a property eligibility check for you instantly.

Ready to Stop Renting?

You don’t need a mountain of cash to buy a home in Texas. Whether it’s through a VA loan, USDA financing, or Texas Down Payment Assistance, homeownership is closer than you think.

At The Josh Brown Team, we specialize in helping families navigate these programs to find the best financial fit. Don’t let the down payment myth hold you back.

Click here to start your complimentary Pre-Approval today or call us at (512) 776-1413 to discuss your options.