How Much House Can I Afford? A Guide for Austin Homebuyers

Buying a home is one of the most exciting milestones in life, especially in a vibrant, growing market like Austin, Texas. Whether you are eyeing a charming bungalow in Hyde Park, a family home in Round Rock, or a new construction in Leander, the first question on every buyer’s mind is usually the same: “How much house can I afford?”

While browsing listings is the fun part, understanding your purchasing power is the critical first step. It saves you from the heartbreak of falling in love with a property that is outside your budget and positions you as a serious buyer in the competitive Austin real estate market.

At The Josh Brown Team, we believe in transparency and education. This guide will walk you through the factors that determine affordability, how the unique Texas property tax landscape affects your monthly payment, and why getting pre-approved is your golden ticket to homeownership.

Understanding the Basics of Home Affordability

When you ask, “How much house can I afford?”, you are essentially asking what monthly mortgage payment fits comfortably within your budget while meeting lender guidelines. It is not just about the sticker price of the home; it is about the components that make up your monthly obligation, often referred to as PITI:

- Principal: The money that goes toward paying down the loan balance.

- Interest: The cost of borrowing the money.

- Taxes: Property taxes (a significant factor in Texas).

- Insurance: Homeowners insurance and, if applicable, Private Mortgage Insurance (PMI).

To determine your maximum purchase price, lenders look at your financial health through a metric called the Debt-to-Income (DTI) ratio.

The Golden Rule: Debt-to-Income (DTI) Ratio

Your DTI ratio is the percentage of your gross monthly income that goes toward paying debts. Lenders look at two types of DTI:

- Front-End Ratio: The percentage of your income that goes specifically toward housing costs (mortgage, taxes, insurance, HOA). Ideally, this should be around 28% or lower.

- Back-End Ratio: The percentage of your income that goes toward all debt obligations, including housing, student loans, car payments, and credit cards. Most lenders prefer this to be 36% to 43%, though some loan programs allow for higher ratios.

For example, if you earn $10,000 a month before taxes, a conservative lender might suggest your total debts (including the new house) shouldn’t exceed $3,600 to $4,300.

The “Texas Factor”: Property Taxes and Insurance

If you are moving to Austin from another state, or even if you are a local first-time buyer, it is crucial to understand how Texas taxes impact affordability. Texas has no state income tax, which is a great financial benefit. However, to balance this, property taxes in Texas are among the highest in the nation.

When using a standard online mortgage calculator, it might estimate taxes at a national average (often 1-1.5%). In the Austin area (Travis, Williamson, and Hays counties), tax rates can range from 1.8% to over 3% depending on the school district and municipal utility districts (MUDs).

Why does this matter?

A $400,000 home with a 2.5% tax rate will have a significantly higher monthly payment than the same priced home in a state with a 1% tax rate. When calculating affordability with The Josh Brown Team, we use realistic local tax rates to ensure you aren’t blindsided by the monthly payment.

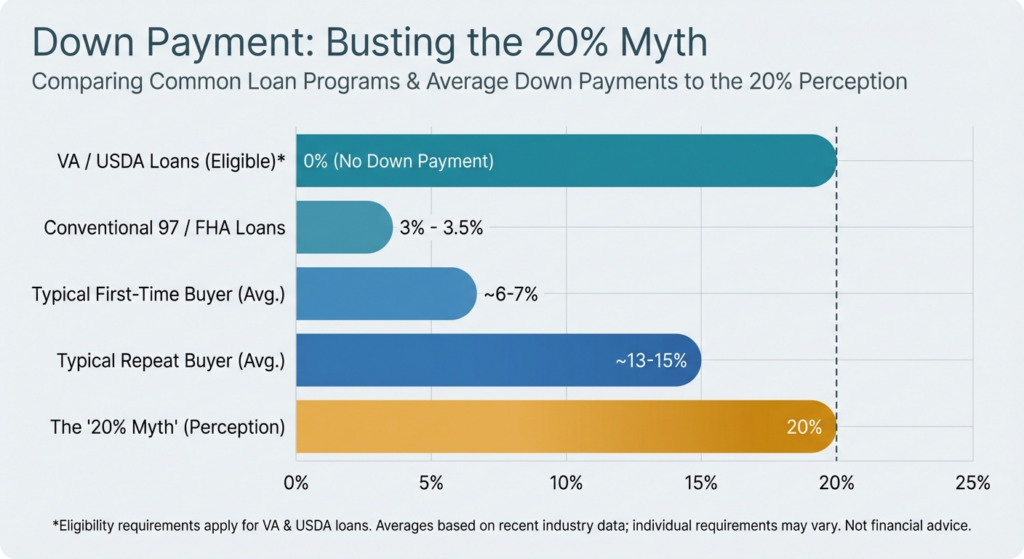

Down Payment: Busting the 20% Myth

One of the biggest misconceptions stopping renters from becoming buyers is the belief that you need a 20% down payment. While putting 20% down helps you avoid Private Mortgage Insurance (PMI), it is not a requirement for buying a home.

Your affordability is heavily influenced by the loan program you choose, as each has different down payment requirements:

- Conventional Loans: often require as little as 3% to 5% down for qualified buyers.

- FHA Loans: A popular choice for first-time buyers, requiring only 3.5% down and offering more flexible credit requirements.

- VA Loans: For eligible veterans and active-duty military, this program offers 0% down payment and no PMI.

- USDA Loans: For homes in designated rural areas (which can include outskirts of the Austin metro), offering 0% down.

- Jumbo Loans: For luxury properties exceeding conforming loan limits, down payment requirements may vary but are competitive.

Understanding which program fits your financial profile is something we specialize in at Fairway Independent Mortgage Corporation.

Affordability Scenarios: The Numbers

To give you a clearer picture, let’s look at how interest rates and down payments affect the monthly principal and interest payment on a home.

Note: The table below estimates Principal and Interest only. It does not include Taxes, Insurance, or HOA fees, which vary by specific property.

Scenario: $450,000 Home Purchase

| Down Payment | Loan Amount | Interest Rate: 6.0% | Interest Rate: 6.5% | Interest Rate: 7.0% |

|---|---|---|---|---|

| 3.5% ($15,750) | $434,250 | $2,603 | $2,744 | $2,889 |

| 5% ($22,500) | $427,500 | $2,563 | $2,702 | $2,844 |

| 10% ($45,000) | $405,000 | $2,428 | $2,560 | $2,694 |

| 20% ($90,000) | $360,000 | $2,158 | $2,275 | $2,395 |

As you can see, a lower interest rate or a larger down payment can significantly impact your monthly obligation. However, waiting to save 20% while home prices in Austin continue to rise might cost you more in the long run than paying PMI for a few years.

Don’t Forget Closing Costs

When asking “How much house can I afford?”, you must also consider the “cash to close.” In addition to your down payment, you will need to pay closing costs. These typically range from 2% to 5% of the loan amount.

Closing costs cover third-party fees such as:

- Appraisal fees

- Title insurance

- Origination fees

- Prepaid items (taxes and insurance to set up your escrow account)

In some market conditions, you may be able to negotiate for the seller to pay a portion of these costs, keeping more cash in your pocket.

The Importance of Pre-Approval in Austin

Online calculators are great for rough estimates, but they cannot evaluate your credit report, verify your income, or account for current market rates. To truly know what you can afford, you need a Pre-Approval.

A pre-approval letter from The Josh Brown Team does two things:

- It defines your budget: You will know exactly how much a lender is willing to lend you, preventing you from looking at homes out of reach.

- It makes you competitive: In the Austin market, sellers rarely entertain offers from buyers who aren’t pre-approved. It shows you have the financial backing to close the deal.

Why Choose The Josh Brown Team?

Josh Brown has consistently been ranked in the Top 25 Lenders in Austin by the Austin Business Journal. We aren’t just a faceless online bank; we are your neighbors.

We know that real estate doesn’t happen between 9 AM and 5 PM. That is why we are available when you are shopping for homes—evenings and weekends. Our goal is to give you clear competitive advantages, weekly updates, and the peace of mind that comes with working with a local expert.

Frequently Asked Questions (FAQs)

1. How accurate are online mortgage affordability calculators?

Online calculators are useful tools for getting a ballpark figure, but they often lack the nuance of your specific financial situation. They may not account for accurate local property taxes, HOA fees, or specific loan program details (like VA or FHA guidelines). For a precise number, it is best to speak with a loan officer.

2. Can I afford a house if I have student loans?

Yes! Having student loans does not automatically disqualify you from buying a home. Lenders look at your Debt-to-Income (DTI) ratio. As long as your total monthly debt payments (including the new mortgage and student loans) fall within the lender’s guidelines, you can still qualify. There are also specific rules for how student loans are calculated that can work in your favor.

3. What is the difference between Pre-Qualification and Pre-Approval?

Pre-qualification is usually a self-reported estimate of what you might be able to borrow. Pre-approval is a verified commitment from a lender based on an analysis of your credit, income, and assets. In the Austin market, a pre-approval letter carries much more weight with sellers.

4. Do I need excellent credit to buy a house in Austin?

While a higher credit score can get you a lower interest rate, you do not need perfect credit to buy a home. FHA loans, for example, allow for credit scores as low as 580 (with a 3.5% down payment). We work with clients to find the best loan product for their credit profile.

5. How do HOA fees affect my affordability?

Homeowners Association (HOA) fees are factored into your Debt-to-Income ratio. If you are looking at a condo downtown or a home in a master-planned community with high HOA dues, it will reduce the amount of monthly mortgage payment you can afford. It is important to check the HOA fees on any property you are interested in.

Ready to Find Your Dream Home?

Determining how much house you can afford is the foundation of a successful home-buying journey. Don’t rely on guesswork. Let The Josh Brown Team at Fairway Independent Mortgage Corporation provide you with a custom analysis tailored to the Austin market.

We are here to help you navigate the numbers, explore your loan options, and get you into your new home with confidence.

Contact us today to start your pre-approval process!

Call us at 512-776-1413 or email josh@joshbrownteam.com.